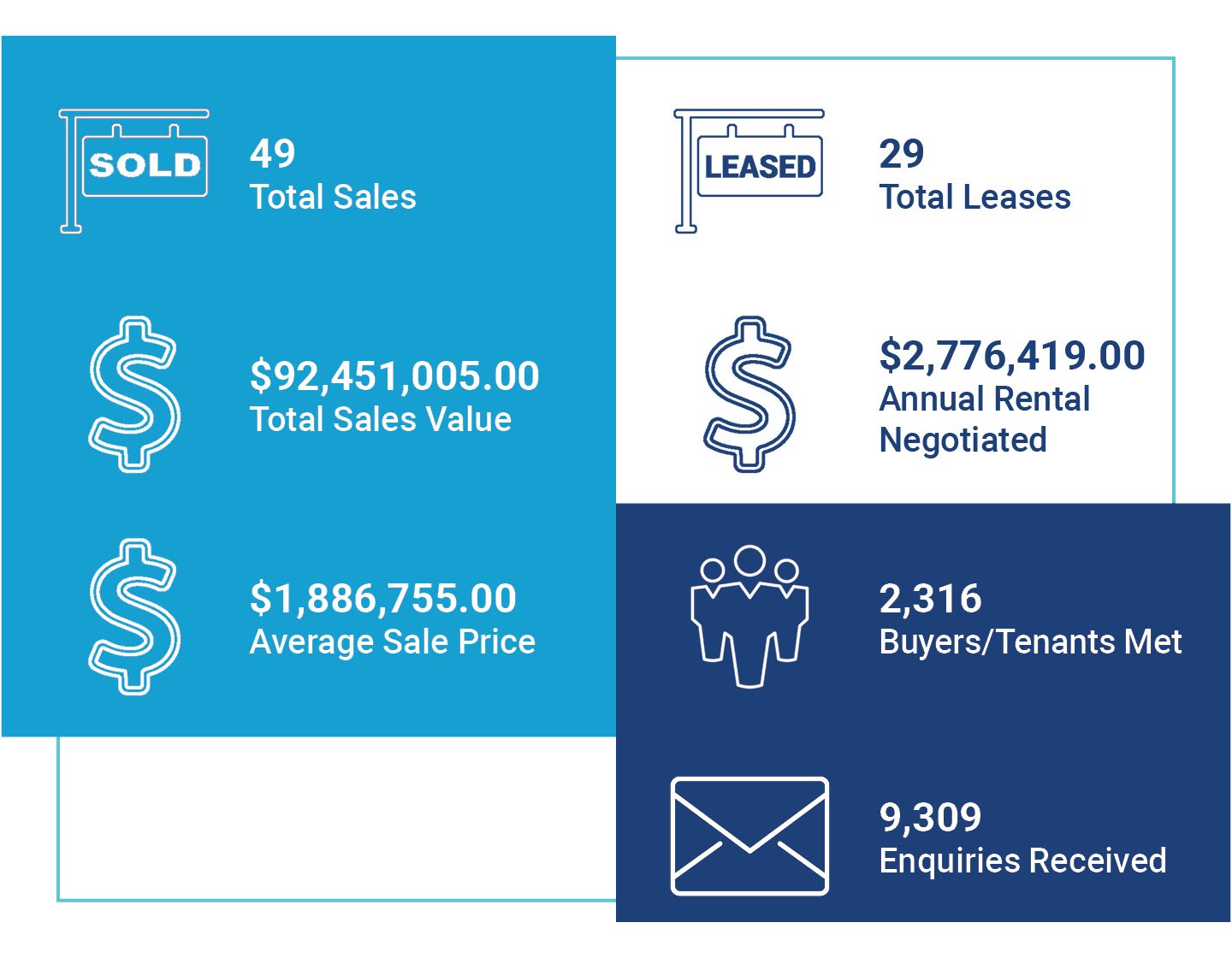

Quarterly Market report - January - March 2025

Dear Clients, Buyers, and Partners,

As we reflect on the 2024 calendar year, the commercial and industrial real estate market across Southern Sydney and the St George region has delivered impressive results. Below is a breakdown of the key trends and insights that shaped the year, highlighting the resilience and strength of this dynamic market.

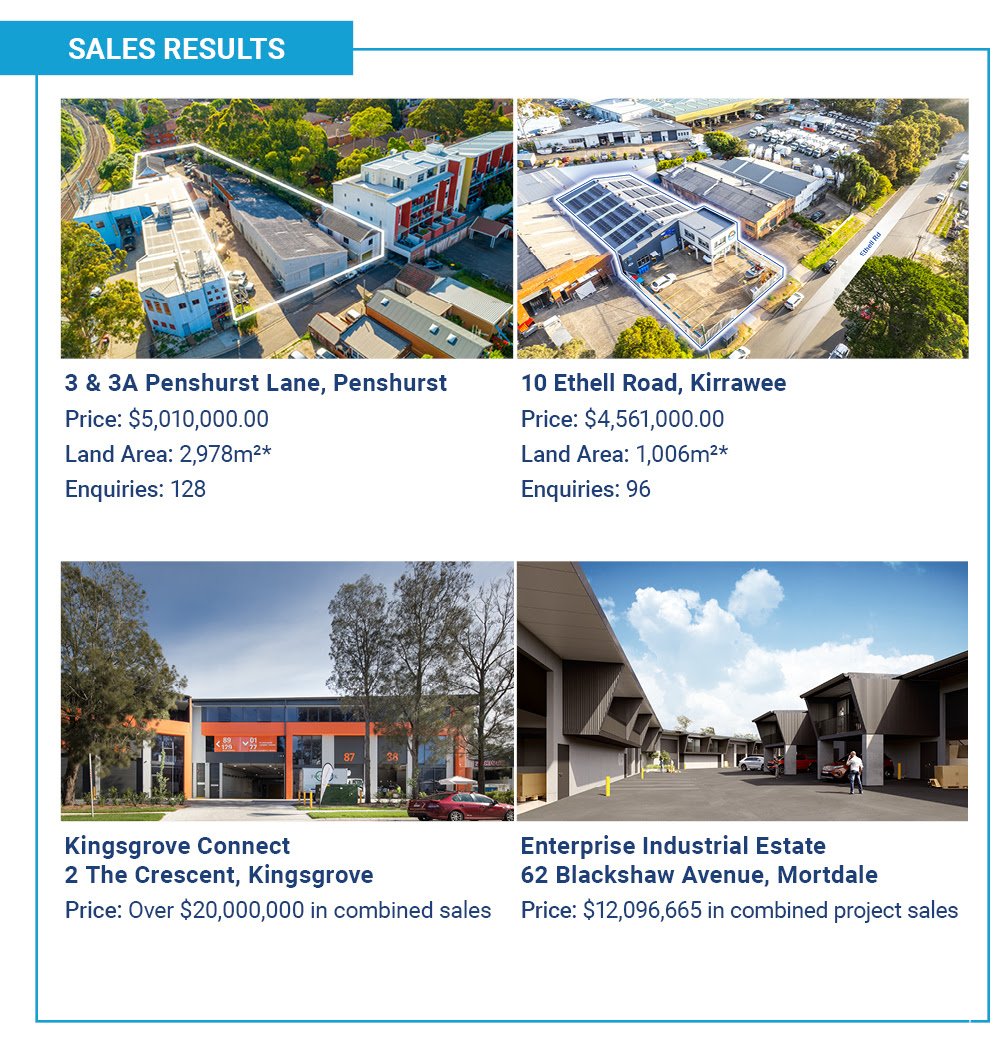

Freehold Industrial Market – Record Highs Amid Limited Supply

The freehold industrial market continued its upward trajectory in 2024, with prices reaching record highs. Limited supply, coupled with relentless demand, has kept competition strong and prices buoyant. New industrial developments brought much-needed stock to the market, further fueling activity in this tightly held sector. Investment in freehold assets remained strong, with sale yields for quality opportunities sitting around 5-5.5% Net, particularly for properties offering future development or refurbishment upside.

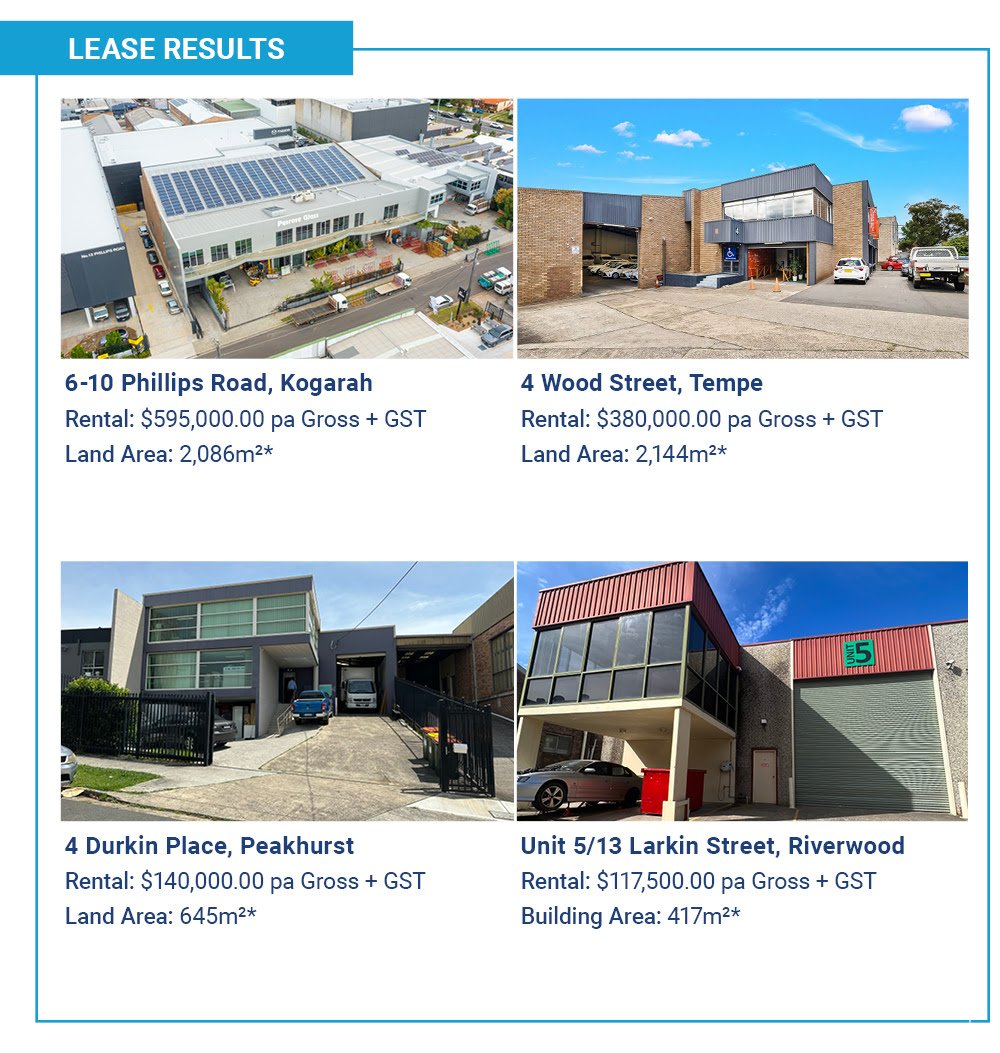

Industrial Leasing – Significant Rental Growth

Industrial leasing experienced a major surge, with rental rates increasing by 10-20% year-on-year. This growth has been driven by:

- Continued undersupply in the region

- High interest rates pushing buyers to lease instead of purchase

- Rising holding costs forcing owners to capitalize on rental demand.

The limited availability of build-to-rent industrial options within Southern Sydney has further amplified competition in the leasing market. While rental growth is expected to continue into 2025, the pace may moderate slightly as the market stabilizes.

Strata Industrial Market – Record Pricing for New Stock & Reductions for Existing

The strata industrial sector hit all-time highs in 2024, with new stock achieving rates between $8,000.00 & $9,000.00/m2. Despite strong supply, the demand for high-quality new developments has kept prices elevated. In contrast, older existing stock has seen some price reductions in areas where new supply has shifted buyer preferences. This trend underscores the importance of quality, location, and modern features in attracting buyers in the current market.

Investment Sales – Resilience Despite Higher Interest Rates

Investment activity remained a key driver of the market, as investors continued to focus on low-risk industrial assets, accepting tighter yields in the current interest rate environment. Sale yields averaged:

- 6-6.5% Net for strata industrial investments

- 5-5.5% Net for premium freehold opportunities with upside potential.

Higher-risk retail and commercial assets saw vendors adjusting their expectations to align with market demand, enabling transactions to occur more effectively.

Development Site Sales – Challenges and Opportunities Ahead

Development site sales were the most impacted market segment in 2024. Increasing construction costs and developers’ reluctance to meet landowners’ high price expectations created a slowdown in activity. However, there remains a clear need for quality residential developments to address Sydney’s housing shortage. As market conditions shift, 2025 may present strong opportunities for development site sales, particularly as more landowners become willing to align with market realities.

A Resilient Market in Challenging Conditions

Despite broader economic challenges, rising operational costs, and elevated interest rates, the demand driven by owner-occupiers and investors alike for quality commercial and industrial properties in Southern Sydney and the St George region has proven resilient, driving growth and keeping prices buoyant in what continues to be one of Sydney’s strongest metropolitan regions.

Thank you for your trust and support throughout 2024. I look forward to partnering with you in the year ahead, navigating the opportunities this dynamic market continues to offer.